I recently commented that dividend investing may be a key part of my retirement plan, but also admitted that I didn’t know much about it.

I recently commented that dividend investing may be a key part of my retirement plan, but also admitted that I didn’t know much about it.

I’m in the midst of studying the strategy, seeing if it has legs, and deciding if I can (and want to) make it a solid part of my retirement plan. To do this, I recently went to my local library and ordered a few books on dividend investing.

Today I’ll share what I’ve learned so far on my journey.

The Concept

From what I understand, proponents of dividend investing tout it as working as follows:

- Buy stocks of good quality companies that pay decent dividends (which would be 3% to 5% these days.)

- Earn income generated from the dividend payments.

- Get some growth on the value of the stocks paying the dividends.

So to make this a bit more tangible, let’s take the following example:

- You buy a portfolio of stocks for $500k.

- These stocks pay you a 4% dividend of $20,000.

- The stocks appreciate 4% over the course of the year and are worth $520,000 at the end of year one.

In this example, your stocks have had a total return of 8% (which is completely reasonable) through the combination of dividends and growth.

Most dividend investors would look for their investments to beat the major market indices. I don’t need to go that far. All I need is some income and enough growth to make up for rising inflation (I’m figuring on 3% income and 3% growth). If I get extra return, that’s great, but I don’t need it.

Five Reasons Why Dividend Investing Works

But that’s my take on why dividend investing works (and how it works). What do the “experts” say? In All About Dividend Investing, Second Edition (All About Series), the authors offer the five reasons why dividend investing works as follows:

1. Dividends provide a steady stream of income.

2. Dividend stock prices increase over time.

3. Dividend reinvestment allows investment to grow at a compounded rate.

4. Dividend reinvestment promotes dollar cost averaging.

5. Dividend-paying stocks generally have lower price volatility.

I especially like the first two since they will be the main reasons I pursue this strategy (if I ultimately decide it does work for me).

Success of Dividend Investing

Continuing on the learning path, I’ve found that there are a seemingly myriad number of ways that dividend stocks can be picked (and even if you use stocks at all — some people suggest mutual funds). But no matter what you use, the advocates for dividend investing seem pretty confident of its success.

Consider this quote from The Motley Fool Million Dollar Portfolio LP: How to Build and Grow a Panic-Proof Investment Portfolio:

And so here’s one key takeaway: Dividend-paying companies are surer bets as investments since, on average, they operate in mature industries and enjoy steady flows of earnings. There is a reason why we have launched our book’s examination of investment strategies by focusing first on dividends — this is the safest way to invest in equities.

And later they say:

A truckload of academic studies has shown that investing in companies that pay dividends is just about the best way to earn huge returns over time.

Again, they are looking at dividend investing compared to all the other investing strategies and saying it’s one of the best. I don’t need it to be one of the best — I have a much lower hurdle to jump. This gives me a margin of safety which I like.

Similar sentiments are given in Beating the S&P with Dividends: How to Build a Superior Portfolio of Dividend Yielding Stocks. They sing the praises of dividend investing as follows:

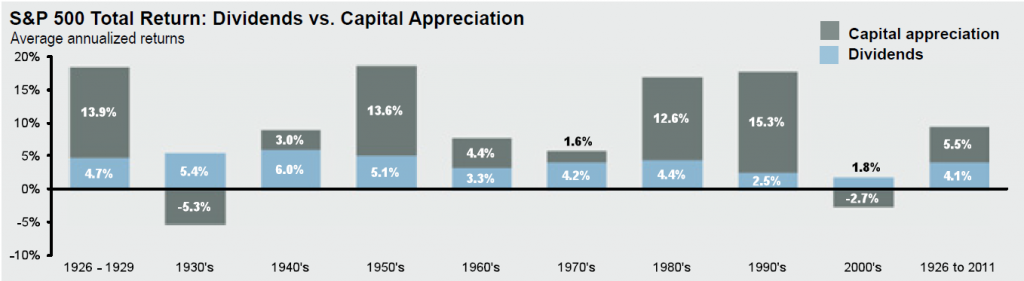

It is a common misconception that most of the returns to investors who invest in stocks have come from capital growth. However, since 1926 nearly half of the 10.3% annual stock market return has come from dividends and dividend reinvestment. As an example, over the past 70 years, ending December 31, 2002, dividends contributed almost 40% of the average annual return of stocks on the S&P 500 Composite Index.

There are a number of formal studies that have found dividend stocks provide higher returns. For example, one study of monthly returns by S&P 500 companies over 31 years found that dividend-paying companies significantly outperformed non-dividend-paying firms by 0.37% per month.

Of course these books have a certain point of view they are trying to sell, so such statements aren’t surprising. That said, the fact that there are studies showing that dividend stocks do well is at least a partial boost for the strategy.

That’s about as far as I’ve gotten into my investigation of the topic. Obviously I still have a long way to go and there’s still a HUGE question out there (how do I find the right stocks that deliver the results I want?) If you have any thoughts on what I should consider as I proceed, I’d love to hear them. Or if you’re a dividend investor yourself, perhaps there are some words of wisdom you can share.